A stock’s volatility under EWMA is estimated at 3.5% on a day its price is $10. The next day, the price moves to $11.

What is the EWMA estimate of the volatility the next day? Assume the persistence parameter = 0.93.

A. 0.0421

B. 0.0224

C. 0.0429

D. 0.0018

Answer: A

Explanation:

The correct answer is choice ‘a’

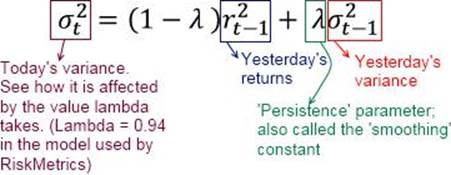

Recall the formula for calculating variance under EWMA. See below. Therefore the correct answer is =SQRT ((1 – 0.93) *(LN (11/10))^2 + 0.93*((3.5%^2))) = 4.21%. Other answers are incorrect. Note that continuous returns are to be used, ie ln (11/10) and not discrete returns (=1/10) – though generally the difference between the two is small over short time periods. (If in the exam the answer doesn’t exactly match, try using discrete returns.)

Latest 8008 Dumps Valid Version with 362 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund