As the persistence parameter under EWMA is lowered, which of the following would be true:

A . The model will react slower to market shocks

B . The model will react faster to market shocks

C . High variance from the recent past will persist for longer

D . The model will give lower weight to recent returns

Answer: B

Explanation:

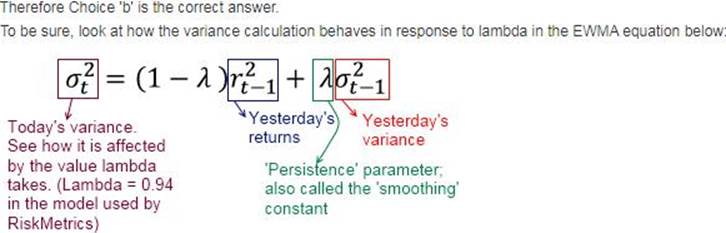

The persistence parameter, , is the coefficient of the prior day’s variance in EWMA

calculations. A higher value of the persistence parameter tends to ‘persist’ the prior value of variance for longer. Consider an extreme example – if the persistence parameter is equal to 1, the variance under EWMA will never change in response to returns.

1 – is the coefficient of recent market returns. As is lowered, 1 – increases, giving a greater weight to recent market returns or shocks. Therefore, as is lowered, the model will react faster to market shocks and give higher weights to recent returns, and at the same time reduce the weight on prior variance which will tend to persist for a shorter period.

Latest 8008 Dumps Valid Version with 362 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund