SIMULATION

Ota L’Abbe, a supervisor at an investment research firm, has asked one of the junior analysts, Andreas Hally, to draft a research report dealing with various accounting issues.

Excerpts from the request are as follows:

• “There’s an exciting company that we’re starting to follow these days. It’s called Snowboards and Skateboards, Inc. They are a multinational company with operations and a head office based in the resort town of Whistler in western Canada. However, they also have a significant subsidiary located in the United States."

• "Look at the subsidiary and deal with some foreign currency issues including the specific differences between the temporal and all-current methods of translation, as well as the effect on financial ratios."

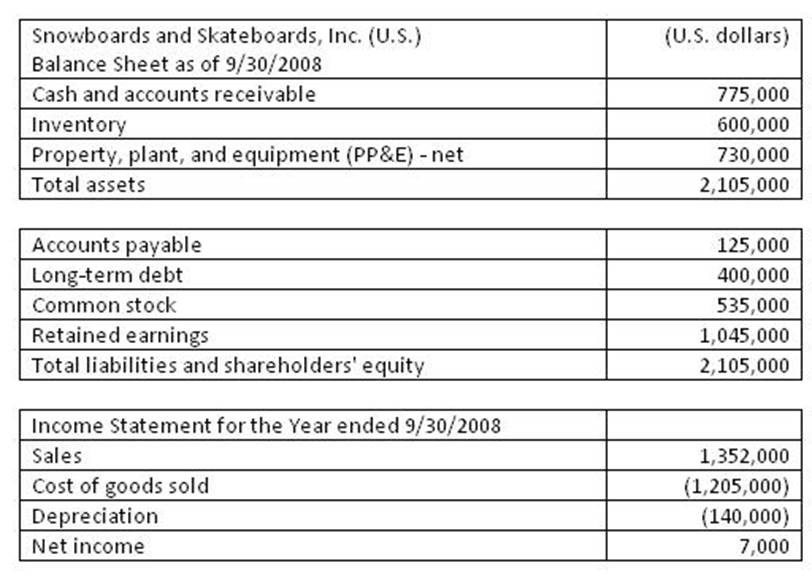

• "The attached file contains the September 30, 2008, financial statements of the U.S. subsidiary. Translate the financial statements into Canadian dollars in a manner consistent with U.S. GAAP."

The following are statements from the research report subsequently written by Hally:

Statement 1: Subsidiaries whose operations are well integrated with the parent will use the all-current method of translation.

Statement 2: Self-contained, independent subsidiaries whose operating, investing, and financing activities are primarily located in the local market will use the temporal method of translation.

Other information to be considered

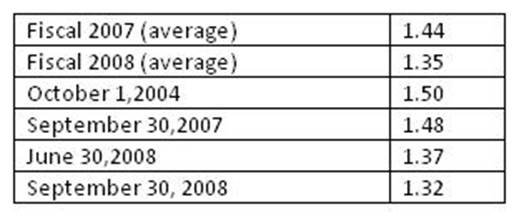

• Exchange rates (CAD/USD)

• Beginning inventory for fiscal 2008 had been purchased evenly throughout fiscal 2007. The company uses the FIFO inventory value method.

• Dividends of USD 25,000 were paid to the shareholders on June 30, 2008.

• All of the remaining inventory at the end of fiscal 2008 was purchased evenly throughout fiscal 2008.

• All of the PP&E was purchased, and all of the common equity was issued at the inception of the company on October 1, 2004. No new PP&E has been acquired, and no additional common stock has been issued since then. However, they plan to purchase new PP&E starting in fiscal 2009.

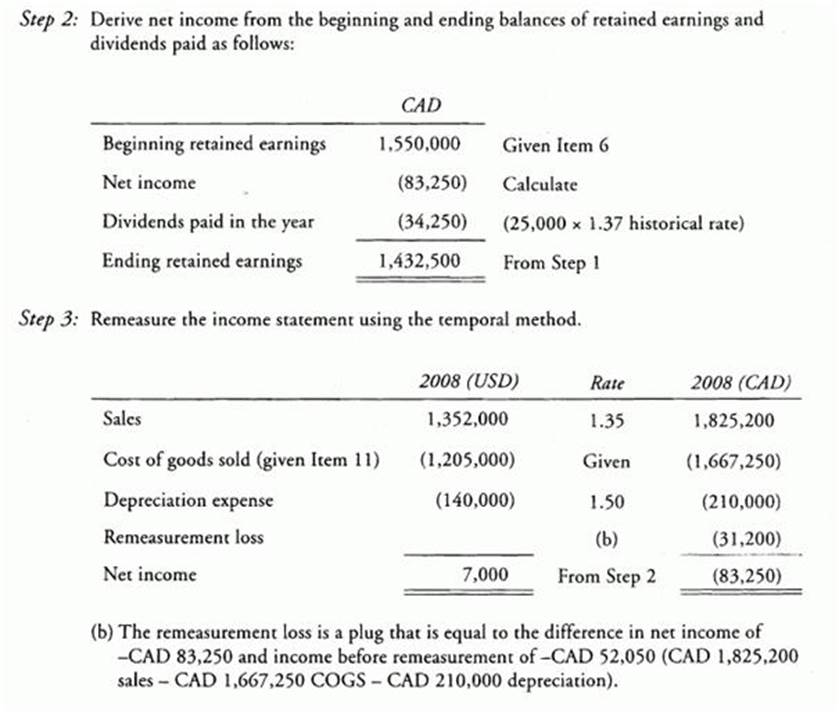

• The beginning retained earnings balance for fiscal 2008 was CAD 1,550,000.

• The accounts payable on the fiscal 2008 balance sheet were all incurred on June 30, 2008.

• The U.S. subsidiary’s operations are highly integrated with the main operations in Canada.

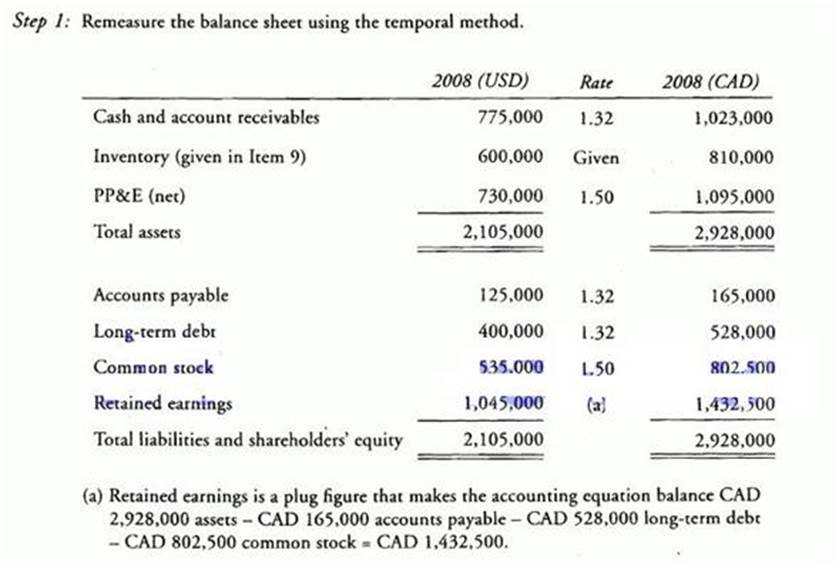

• The remeasured inventory for 2008 using the temporal method is CAD 810,000.

• All monetary asset and liability balances are the same as they were at the end of the 2007 fiscal year, except that long-term debt was USD 467,700.

• Costs of goods sold under the temporal method in 2008 is CAD 1,667,250.

Using the appropriate translation method, which of the following best describes the effect of changing exchange rates on the parent’s fiscal 2008 financial statements?

A . An accumulated loss of CAD 242,100 is reported in the shareholders’ equity.

B . A loss of CAD 31,200 is recognized in the income statement.

C . A gain of CAD 27,400 is recognized in the income statement.

Answer: B

Explanation:

Use the following to answer this question.

The Canadian dollar is the functional currency because the subsidiary is highly integrated with the parent. Therefore, the temporal method applies.

Since the subsidiary’s operations are highly integrated with the parent, the temporal method is used. Accordingly, a loss of CAD 31,200 is recognized in the parent’s income statement (see balance sheet and income statement worksheet).

However, no calculations are actually necessary to answer this question. The parent has a net monetary asset position in the subsidiary (monetary assets > monetary liabilities). Holding net monetary assets when the foreign currency is depreciating will result in a loss. Under the temporal method, the loss is reported in the income statement. Only choice B satisfies this logic. (Study Session 6, LOS 23.d)

Latest CFA Level 2 Dumps Valid Version with 713 Q&As

Latest And Valid Q&A | Instant Download | Once Fail, Full Refund