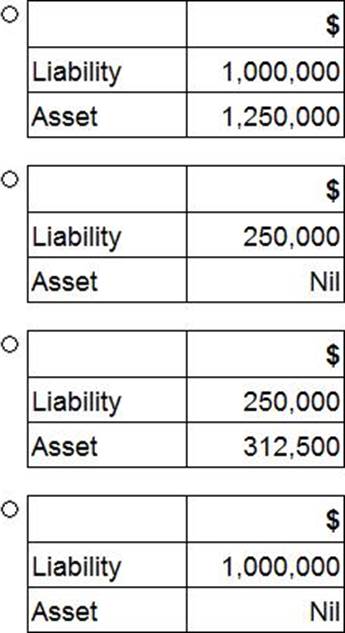

JKL measure gearing as debt:equity, based on book values. At 31 December 20X5 the ratio is 2:3 and JKL would like this to be 2:5.

Which of the following transactions individually would achieve this?

- A . Bonus issue from the share premium account.

- B . Revaluation of investment property to an increased fair value.

- C . Repayment of a 6 year term loan with the issue of 5 year redeemable debentures.

- D . Issue of redeemable preference shares at par.

LM acquired an asset under a 5-year non-cancellable operating lease agreement on 1 January 20X8. Under the terms of the agreement, LM paid nothing for the first year and then made four payments of $50,000 in each subsequent year. LM adopted the provisions of IAS 17 Leases when accounting for this agreement.

Which of the following is correct in respect of this operating lease in LM’s financial statements for the year to 31 December 20X8?

- A . An accrual of $40,000 was recognised.

- B . An accrual of $50,000 was recognised.

- C . A prepayment of $10,000 was recognised.

- D . An expense of $50,000 was recognised.

Entity A entered into a 3 year operating lease on 1 April 20X3. The rentals are £5,000 a year payable in advance with an additional payment of $1,800 payable on 1 April 20X3.

The rental expense to be included in the statement of profit or loss for the year ended 31 December 20X3 will be:

- A . $4,200

- B . $5,000

- C . $6,800

- D . $5,600

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years’ time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classifed as which of the following?

- A . Compound instrument

- B . Debt instrument

- C . Equity instrument

- D . Discounted instrument

CORRECT TEXT

Which of the following is the correct calculation for basic earnings per share in accordance with IAS 33 Earnings Per Share?

Which THREE of the following actions should improve the cash position of an entity?

- A . Substituting a bonus issue for the final dividend.

- B . Selling non current assets and leasing them back under operating leases.

- C . Implementing an efficient inventory ordering system.

- D . Revaluing all non-current assets.

- E . Revising the depreciation policy of non-current assets.

- F . Offering extended credit terms to existing customers.

Which of the following reduce the usefulness of ratio analysis when comparing entities that operate in the same industry? Select ALL that apply.

- A . The revenue figure being aggregated from many different activities and sources.

- B . Accounting estimates in respect of depreciation being different between entities.

- C . The effect of a material and unusual item being disclosed separately in the notes.

- D . An entity adopting a policy of revaluing its non current assets.

- E . Ratio calculations being based on historical information.

- F . Ratios being quick and easy to calculate.

CORRECT TEXT

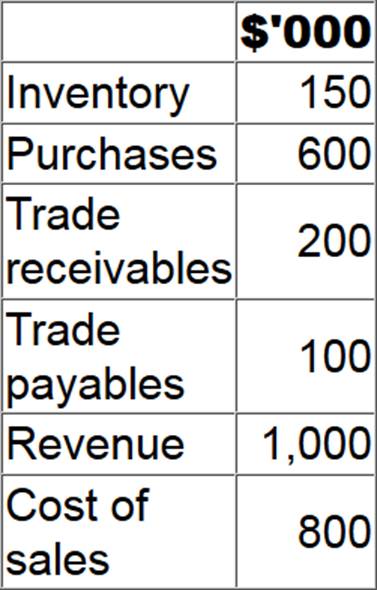

The following information has been extracted from the financial records of DEF for the year ended 31 December 20X2.

What is the operating cycle of DEF at 31 December 20X1?

Assume there are 365 days in the year.

All workings should be rounded to whole days.

Give your answer in whole days.

? days.

BC are currently seeking to establish an accounting policy for a particular type of transaction.

There are four alternative ways in which this transaction can be treated.

Each treatment will have a different outcome on the financial statements as follows:

• Treatment one means that the financial statements will be easier to prepare.

• Treatment two will give a fair representation of the transaction in the financial statements.

• Treatment three will maximise the profit figure presented in the financial statements.

• Treatment four means that the financial statements will be more easily understood by shareholders.

Which accounting treatment should BC adopt?

- A . One

- B . Two

- C . Three

- D . Four

On1 September 20X3, GH purchased 200,000 $1 equity shares in QR for $1.20 each and classified this investment as held for trading.

GH paid a 1% transaction fee to its broker on this transaction. QR’s equity shares had a fair value of $1.35 each on 31 December 20X3.

Which of the following journals records the subsequent measurement of this financial instrument at 31 December 20X3?

- A . Option A

- B . Option B

- C . Option C

- D . Option D

On 1 January 20X4 JK had 1,500,000 ordinary shares in issue. On 1 September 20X4 JK issued 600,000 ordinary shares at the market value of $2.50 a share. For the financial year ended 31 December 20X4 the statement of profit or loss shows profit before tax of $625,000 and profit after tax of $500,000.

What is the earnings per share for the year ended 31 December 20X4?

- A . 23.8 cents

- B . 36.8 cents

- C . 26.3 cents

- D . 29.4 cents

Which TWO of the following statements about bonds and their issue are true?

- A . Credit rating agencies assign risk categories to bond issues.

- B . Bonds are a form of loan capital, traded on stock exchanges.

- C . Bonds are a risk-free form of investing because they will always be repaid.

- D . All bonds have the same terms and conditions when issued.

- E . A bond issue is never underwritten because the return is fixed and guaranteed.

CORRECT TEXT

LK acquired 100% of the equity shares of TU on 1 January 20X4. LK disposed of 60% of TU for £2,400,000 on 30 September 20X4. The sale proceeds reflected the fair value of TU’s shares on that date.

The remaining 40% shareholding gave LK the ability to exercise significant influence

over the activities of TU. TU reported profit of $1,800,000 for the year ended 31 December 20X4 and this accrued evenly throughout the year.

Calculate the investment in associate that will be presented in LK’s consolidated statement of financial position as at 31 December 20X4.

Give your answer to the nearest whole $’000.

$ 000

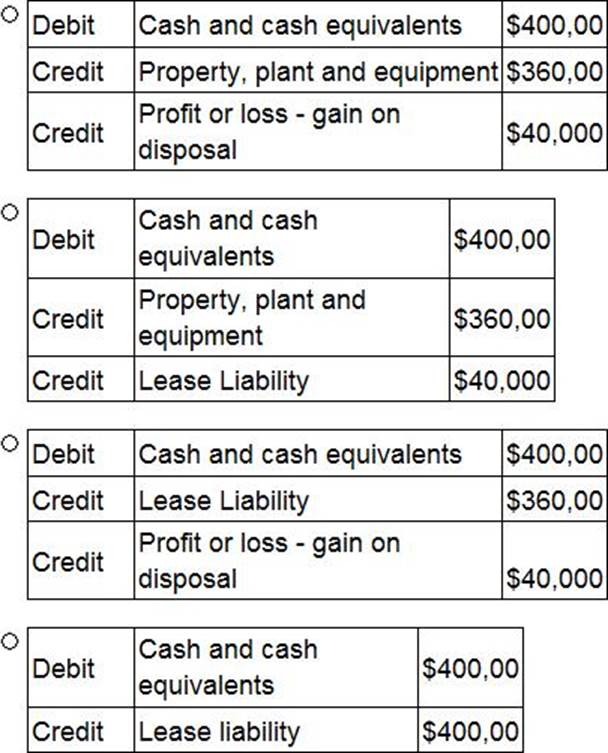

ST has sold its main office property, which had a carrying value of $360,000, to AB, a property management entity.

The property was sold for $400,000 which is equal to its fair value and was immediately leased back under an operating lease agreement.

Which of the following journals will record this transaction?

- A . Option A

- B . Option B

- C . Option C

- D . Option D

Which of the following options provides a representation of how the non controlling interest in FG is measured in CD’s consolidated statement of financial position at 31 December 20X8?

- A . • FV of NCI at acquisition; plus

• NCI’s share of post acquisition reserves of FG; plus

• NCI’s share of accumulated exchange differences arising on goodwill of FG. - B . • FV of NCI at acquisition; plus

• NCI’s share of post acquisition reserves of FG; plus

• NCI’s share of exchange difference arising on goodwill of FG for the year. - C . • FV of NCI at reporting date; plus

• NCI’s share of post acquisition reserves of FG; plus

• NCI’s share of exchange difference arising on goodwill of FG for the year. - D . • FV of NCI at reporting date; plus

• NCI’s share of group reserves; plus

• NCI’s share of accumulated exchange differences arising on goodwill of FG.

As at 31 October 20X7 TU’s financial statements show the entity having profit after tax of $600,000 and 900,000 $1 ordinary shares in issue. There have been no issues of shares during the year. At 31 October 20X7 TU have 300,000 share options in issue, which allow the holders to purchase ordinary shares at $2 a share in 3 years’ time. The average price of the ordinary shares throughout the year was $5 a share.

What is the diluted earnings per share for the year ended 31 October 20X7?

- A . 66.7 cents

- B . 58.8 cents

- C . 50.0 cents

- D . 55.6 cents

On 30 November 20X9 OPQ acquires a financial asset that is classified as Available for Sale.

Which of the following describes the value of the financial asset on the date of acquisition?

- A . Fair value excluding transaction costs.

- B . Fair value including transaction costs.

- C . Present value including transaction costs.

- D . Present value excluding transaction costs.

GG’s gearing is currently 50% compared to the industry average of 40% (both measured as debt/equity). GG’s debt is all in the form of a single bank loan that is repayable in five years’ time. The directors of GG are seeking to raise finance for a new project and they are considering an additional bank loan from the same bank.

Which of the following would prevent the bank from lending the finance for the project in the form of a new bank loan?

- A . A covenant on the existing bank loan that restricts the level of dividend that can be paid.

- B . A projected decrease in interest cover that would breach a covenant on the existing loan.

- C . The revaluation of GG’s property that shows an increase in its value since the existing bank loan was taken out.

- D . A projected lack of profits to be able to claim tax relief on the additional interest arising from the new loan.

CORRECT TEXT

YZ issued $100,000 6% convertible bonds at par on 1 January 20X5. The bondholders have the option to convert into equity shares in 3 years’ time or redeem at par for cash on the same date.

Interest is paid annually in arrears and bonds issued by similar entities without conversion rights pay interest at 8%.

What is the value of equity to be recognised in YZ’s statement of financial position as at 31 December 20X5?

Give your answer to the nearest whole $.

$?

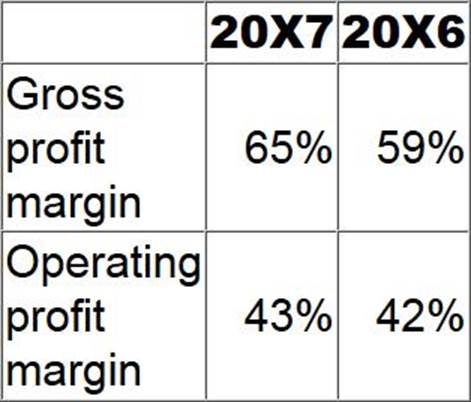

Taking each statement individually, which of the following explains the movement in the gross profit margin from 20X4 to 20X5 as calculated by the analysts?

- A . Increase in the levels of closing inventory of raw materials.

- B . Reduction in the cost of raw materials NOT passed onto customers.

- C . Prompt payment discounts no longer offered to customers.

- D . Increase in the volume of sales over the year.

When accounting for a finance lease under IAS 17 Leases, which TWO of the following are recognised in the statement of profit or loss?

- A . Finance cost element of the lease payments

- B . Depreciation of the leased asset

- C . Lease payments paid

- D . Lease payments payable

- E . Capital repayment element of the lease payments

Which of the following is NOT an example of an unconsolidated structured entity as defined in IFRS12 Disclosure of Interests in Other Entities?

- A . A post-employment benefit plan

- B . A securitisation vehicle

- C . An asset-backed financing scheme

- D . An investment fund

CORRECT TEXT

LK acquired 100% of the equity shares of TU on 1 January 20X4. LK disposed of 60% of TU for £2,400,000 on 30 September 20X4. The sale proceeds reflected the fair value of TU’s shares on that date.

The remaining 40% shareholding gave LK the ability to exercise significant influence over the activities of TU. TU reported profit of $1,800,000 for the year ended 31 December 20X4 and this accrued evenly throughout the year.

Calculate the investment in associate that will be presented in LK’s consolidated statement of financial position as at 31 December 20X4.

Give your answer to the nearest whole $’000.

$ 000

Which TWO of the following are true in relation to IAS21.

The Effects of Changes in Foreign Exchange Rates when consolidating an overseas subsidiary?

- A . A current period exchange gain or loss is shown within the consolidated statement of comprehensive income within other comprehensive income.

- B . Goodwill is re-translated at the end of each reporting period and reflected at the period end exchange rate in the consolidated statement of financial position.

- C . Assets and liabilities of the subsidiary are translated at each reporting date using the average exchange rate for the period.

- D . Goodwill is reflected in the consolidated statement of financial position translated at the exchange rate on the date of acquisition.

- E . The statement of profit or loss of the subsidiary is translated for the reporting period using the closing exchange rate.

On 1 January 20X7 GH purchased plant and equipment at a cost of $400,000. The temporary differences in respect of this plant and equipment at 31 December 20X7 and 20X8 have been calculated as follows:

Assume that there are no other temporary differences in the periods and that the corporate income tax rate is 25%. GH is expected to have significant taxable profits in the future.

Which of the following is the correct impact in GH’s statement of financial position at 31 December 20X8 in respect of deferred tax?

- A . Increase in the deferred tax asset.

- B . Increase in the deferred tax liability.

- C . Decrease in the deferred tax asset.

- D . Decrease in the deferred tax liability.

XY has a weighted average cost of capital (WACC) of 10% based on its gearing level (measured as debt/debt+equity) of 40%. It is considering a signficant new project.

In which of the following situations would it be appropriate to appraise this project using XY’s existing WACC of 10%?

- A . The project is in a different industry to XY’s current operations and funded entirely by equity.

- B . The project is an extension of XY’s current operations and is funded 40% by debt and 60% by equity.

- C . The project is an extension of XY’s current operations and is funded by equal amounts of debt and equity.

- D . The project is in a different industry to XY’s current operations and is funded by equal amounts of debt and equity.

Which of the following reduce the usefulness of ratio analysis when comparing entities that operate in the same industry?Select ALL that apply.

- A . The revenue figure being aggregated from many different activities and sources.

- B . Accounting estimates in respect of depreciation being different between entities.

- C . The effect of a material and unusual item being disclosed separately in the notes.

- D . An entity adopting a policy of revaluing its non current assets.

- E . Ratio calculations being based on historical information.

- F . Ratios being quick and easy to calculate.

AB owned 80% of the equity share capital of FG at 1 January 20X6. AB disposed of 10% of FG’s equity share capital on 31 December 20X6 for $400,000. The non controlling interest was measured at $700,000 immediately prior to the disposal.

Which of the following represents the adjustment that AB made to non controlling interest in respect of the disposal when it prepared its consolidated financial statements at 31 December 20X6?

- A . Credit of $350,000

- B . Debit of $400,000

- C . Debit of $350,000

- D . Credit of $50,000

HJ is currently in dispute with an employee, who is claiming $400,000 in a legal case against them.

HJ’s legal advisors have stated that it is probable that they will lose the case and will have to pay the amount claimed.

Also, HJ are claiming $250,000 from a supplier of defective goods and the legal advisors have stated that it is probable that HJ will be successfulin this claim.

What is the correct accounting treatment for these two items in HJ’s financial statements?

- A . Provide for the $400,000 potential outflow and disclose the $250,000 potential inflow.

- B . Provide for the $400,000 potential outflow and recognise the $250,000 potential inflow.

- C . Disclose the $400,000 potential outflow and disclose the $250,000 potential inflow.

- D . Disclose the $400,000 potential outflow and recognise the $250,000 potential inflow.

Which THREE of the following statements are true in relation to financial assets designated as fair value through profit or loss under IAS 39 Financial Instruments:

Recognition and Measurement?

- A . Shares in another entity held for short term trading purposes fall within this category.

- B . Transaction costs in relation to these assets are expensed to profit or loss on acquisition.

- C . Transaction costs in relation to these assets are added to the initial cost of the asset on acquisition.

- D . The gain or loss on the subsequent measurement of these assets is recorded within other comprehensive income.

- E . The gain or loss on the subsequent measurement of these assets is recorded within profit for the year.

- F . Once the asset has been subsequently measured to fair value an impairment review is undertaken.

CORRECT TEXT

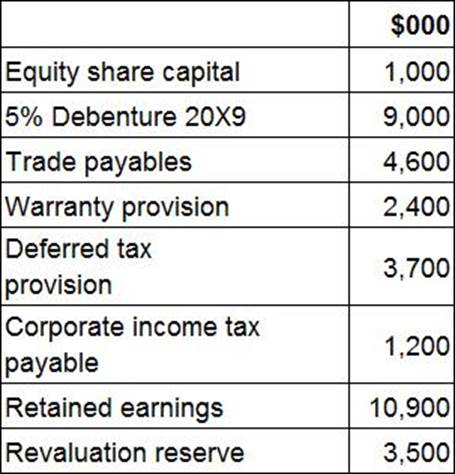

Information extracted from JK’s statement of financial position for the year ended 31 May 20X5 is as follows:

Calculate the gearing ratio (Debt/Equity measured as a percentage) at 31 May 20X5.

Give your answer to one decimal place.

? %

An accountant acting under their Code of Ethics would do which THREE of the following?

- A . Resist pressure from the directors to recognise revenue on sales where the risks and rewards have not transferred to the customer.

- B . Report material conflicts of interest to a more senior level.

- C . Reject a justified change to a depreciation policy that increases profitability.

- D . Accept a recommendation from the audit committee to increase segregation of duties within the finance department.

- E . Make a provision for a liability of uncertain timing or amount, requested by the directors, where there is NOT a present obligation.

- F . Accept a director’s instruction to remove one element of their remuneration from the directors’ remuneration report.

What is meant by the term "a placing of ordinary shares"?

- A . Selling new ordinary shares to a financial institution on a pre-arranged basis.

- B . Selling new ordinary shares directly to the public.

- C . Selling existing ordinary shares to new investors through a stock exchange.

- D . Selling new ordinary shares to existing shareholders.

CORRECT TEXT

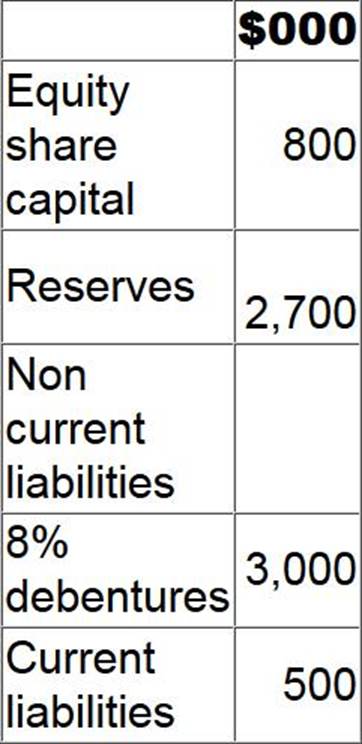

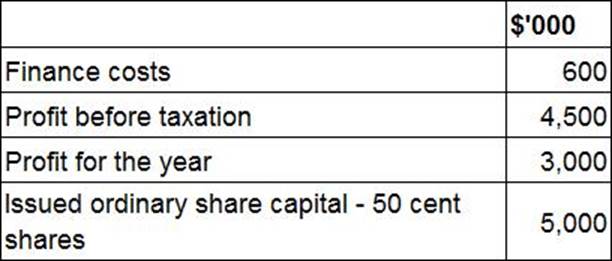

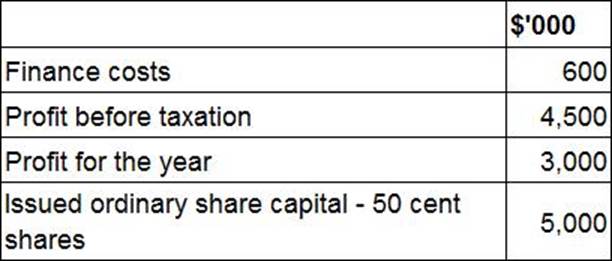

F has profit before interest and tax of $400,000 for the year to 30 June 20X4.

Extracts from F’s statement of financial position at 30 June 20X4 are as follows:

Calculate the gearing (debt:equity) ratio at 30 June 20X4.

Give your answer to the nearest whole percentage.

? %

The directors of AB want to reduce the entity’s gearing ratio in the year to 31 December 20X9.

Which of the following independent actions could the directors take during 20X9 to achieve this?

- A . Recognise the valuation surplus on AB’s property, plant and equipment.

- B . Issue cumulative preference shares.

- C . Issue redeemable preference shares.

- D . Switch AB’s fixed interest bearing borrowing to a lower variable rate borrowing.

Information from the financial statements of RST for the year ended 30 April 20X9 is as follows:

At 30 April 20X9 the ordinary shares are trading at $4.75.

What is the price earnings (P/E) ratio for RST at 30 April 20X9?

- A . 15.83

- B . 7.92

- C . 10.56

- D . 9.31

Information from the financial statements of an entity for the year to 31 December 20X5:

The gearing ratio calculated as debt/equity and interest cover are:

- A . gearing of 15% and interest cover of 6.

- B . gearing of 16% and interest cover of 6.

- C . gearing of 15% and interest cover of 4.

- D . gearing of 16% and interest cover of 4.

LM is preparing its consolidated financial statements for the year ended 30 April 20X5. During the year LM acquired 30% of the equity shares of AB giving it significant influence over AB.

LM conducted ratio analysis comparing the financial performance of the group for 30 April 20X4 and 20X5.

Which of the following ratios would not be comparable as a result of the acquisition of AB?

- A . Operating profit margin.

- B . Return on capital employed.

- C . Earnings per share.

- D . Interest cover.

Which TWO of the following are TRUE in respect of preparing a consolidated statement of cash flows where there has been an acquisition of a subsidiary part way through the year?

- A . Investing activities will include a total cash outflow for the acquisition comprising the cash paid for the subsidiary less the cash held by the subsidiary at the acquisition date.

- B . The working capital held by the subsidiary at acquisition will be excluded from the year end figures based on the percentage shareholding in the subsidiary.

- C . Non-controlling interest will arise in relation to the subsidiary and any dividends paid to the non-controlling interest will be shown within financing activities as a cash outflow.

- D . Any shares that were issued on acquisition of the subsidiary will be shown separately on the statement of cash flows within financing activities.

- E . The year end cash and cash equivalents balance will be reduced by the cash and cash equivalents that were held by the subsidiary at the acquisition date.

CORRECT TEXT

ST acquired 80% of the equity shares of AB on 1 January 20X7. AB acquired 60% of the equity shares of UV on 1 January 20X8. Profit for the year ended 31 December 20X9 for AB is $160,000 and for UV is $100,000.

Calculate the non-controlling interest figure to be included within ST’s consolidated statement of profit or loss for the year ended 31 December 20X9.

Give your answer to the nearest whole number in $000s.

$ ?

Information from the financial statements of RST for the year ended 30 April 20X9 is as follows:

What is the price earnings (P/E) ratio for RST at 30 April 20X9?

- A . 15.83

- B . 7.92

- C . 10.56

- D . 9.31

LM acquired 80% of the equity shares of ST when ST’s retained earnings were $50 million.

The fair value of the net assets of ST included a contingent liability with a fair value of $100 million at the date of acquisition and a fair value of $40 million at 31 December 20X6.

No other fair value adjustments were required at the date of acquisition.

LM and ST had retained earnings of $200 million and $80 million respectively at 31 December 20X6.

The consolidated retained earnings of LM at 31 December 20X6 were:

- A . $164 million

- B . $176 million

- C . $272 million

- D . $284 million

When accounting for a finance lease under IAS 17 Leases, which TWO of the following are recognised in the statement of profit or loss?

- A . Finance cost element of the lease payments

- B . Depreciation of the leased asset

- C . Lease payments paid

- D . Lease payments payable

- E . Capital repayment element of the lease payments

CORRECT TEXT

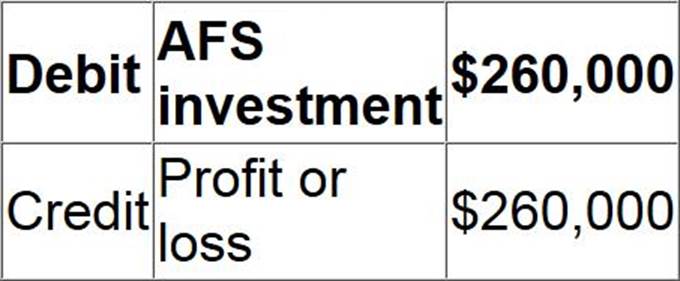

KL acquired 2 million $1 equity shares in MN on 18 July 20X0 for $1.65 a share and classified this investment as available for sale (AFS) in accordance with IAS 39 Financial instruments: Recognition and Measurement.

KL paid a 0.5% transaction fee to its broker on this transaction. MN’s shares were trading at $1.78 on 31 December 20X0.

Which of the following journals records the subsequent measurement of this investment at 31 December 20X0?

GH owned 70% of the equity share capital of XY at 1 January 20X6. GH acquired a further 20% of XY’s equity share capital on 31 December 20X6 for $430,000. Non controlling interest was measured at $600,000 immediately prior to the 20% acquisition.

Which of the following amounts will GH debit to non controlling interest when the 20% acquisition is adjusted for in its consolidated financial statements at 31 December 20X6?

- A . $400,000

- B . $120,000

- C . $200,000

- D . $430,000

How would KL account for its investment in MN in its consolidated financial statements for the year to 31 December 20X9?

- A . Joint venture

- B . Joint arrangement

- C . Financial asset

- D . Subsidiary

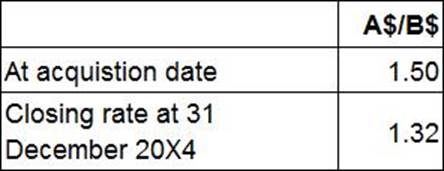

A group presents its financial statements in A$.

The goodwill of its only foreign subsidiary was measured at B$100,000 at acquisition.

There have been no impairments to this goodwill.

Exchange rates (where A$/B$ is the number of B$’s to each A$) are as follows:

The value of goodwill to be included in the group’s statement of financial position in respect of its foreign subsidiary for the year ended 31 December 20X4 is:

- A . A$75,758.

- B . A$66,667.

- C . A$150,000.

- D . A$132,000.

ST acquired 75% of the 2 million $1 equity shares of CD on 1 January 20X3, when the retained earnings of CD were S3,550,000. CD has no other reserves.

ST paid $5,600,000 for the shares in CD and the non controlling interest was measured at its fair value of S1,400,000 at acquisition.

At 1 January 20X3, the fair value of CD’s net assets were equal to their carrying amount, with the exception of a building. This building had a fair value of $1,000,000 in excess of its carrying amount and a remaining useful life of 25 years on 1 January 20X3.

At 31 December 20X5, the retained earnings of ST and CD were $8,500,000 and $5,250,000 respectively.

What is the value of retained earnings that will be presented in the consolidated statement of financial position of ST as at 31 December 20X5?

- A . $9,685,000

- B . $9,775,000

- C . $9,715,000

- D . $10,080,000

On 1 January 20X1 KL acquired 75% of the equity shares of PQ. Goodwill arising on the acquisition was $480,000. On 31 December 20X3 KL sold the full investment of PQ to XY Group for $2,000,000. On this date the net assets of PQ were $1,340,000 and the non-controlling interests stood at $410,000.

What is the gain on disposal to be recognised in the consolidated statement of profit or loss of KL?

- A . $590,000

- B . $180,000

- C . $660,000

- D . $635,000

AB and CD are separate entities that prepare financial statements to 31 May using international accounting standards. AB and CD provide technical support services to the financial services industry and operate in the same country.

The financial statements are identical except for the following:

• AB purchased all operating equipment, paying $100,000, using a 5 year bank loan. The useful life of the equipment was 5 years.

• CD signed an operating lease agreement for all operating equipment for 5 years paying $20,000 per year.

Both entities charge all expenses relating to the equipment to cost of sales.

From the information provided, which of the following ratios would be reliably comparable for AB andCD?

- A . Gross profit margin

- B . Return on capital employed

- C . Non current asset turnover

- D . Profit before tax margin

EF obtained a government licence, free of charge, to operate a silver mine in 20X7 and $5 million was spent on preparing the site. The mine commenced operation on 1 January 20X8. The licence requires that at the end of the mine’s useful life of 20 years, the site above ground must be reinstated to its original position.

EF estimated that the cost in 20 years’ time of this reinstatement will be $3 million, which has a present value of $1 million at 1 January 20X8.

Which THREE of the following describe how the cost of the reinstatement of the site should be treated in the financial statements of EF in the year ended 31 December 20X8?

- A . The cost of the mine will be increased by $1 million on 1 January 20X8.

- B . The cost of the mine will be increased by $3 million on 1 January 20X8.

- C . There will be a credit to finance costs for the unwinding of the discount on the reinstatement provision.

- D . There will be a debit to finance costs for the unwinding of the discount on the reinstatement provision.

- E . Only the cost of the site preparation will be depreciated over the mine’s useful economic life.

- F . Depreciation will be charged over 20 years on the full cost of the mine including the reinstatement cost.

The following information relates to DEF for the year ended 31 December 20X7:

• Property, plant and equipment has a carrying value of $3,500,000 and a tax written down value of $2,500,000.

• There are unused tax losses to carry forward of $1,250,000. These tax losses have arisendue topoor trading conditions which are not expected to improve in the foreseeable future.

• The corporate income tax rate is 25%.

In accordance with IAS 12 Income Taxes, the financial statements of DEF for the year ended 31 December 20X7 would recognise deferred tax balances of:

- A . Option A

- B . Option B

- C . Option C

- D . Option D

GH acquired 3,000,000 of the 12,000,000 equity shares of JK. All shares carried equal voting rights and no other single shareholder of JK held more than 10% of the equity shares. GH has the power to participate in the financial and operating policy decisions but not control them.

Based on the information provided above, how would GH’s investment in JK be accounted for in its consolidated financial statements?

- A . Associate

- B . Joint venture

- C . Joint arrangement

- D . Financial asset

AB acquired its one subsidiary, CD, on 1 January 20X1. At this date the fair value of CD’s property, plant and equipment was found to be $40 million higher than its carrying value. The relevant items had a remaining estimated useful life of 10 years from the date of acquisition.

At 31 December 20X4 AB and CD presented property, plant and equipment of $100 million and $50 million respectively in their individual financial statements.

The value of property, plant and equipment presented in AB’s consolidated statement of financial position at 31 December 20X4 is:

- A . $174 million

- B . $190 million

- C . $150 million

- D . $134 million

ST has in issue unquoted 7% debentures which were issuedat par and are redeemable in 1 year’s time. These debentures cannot be traded. The yield to maturity on these debentures has been calculated at 5%.

Which of the following would explain why the yield to maturity is lower than the coupon?

- A . ST will benefit from the tax relief on the interest payment.

- B . The debentures will be redeemed at a discount to their par value.

- C . The debentures will be redeemed at their par value.

- D . The market value of the debentures must be higher than their par value.

AB, a listed entity, prepared its financial statements to 31 December 20X7, in accordance with international accounting standards.

Which THREE of the following were disclosed as related parties of AB in its financial statements?

- A . AB’s defined benefit pension plan.

- B . The wife of the Managing Director of AB, to whom AB sold a motor vehicle in the year to 31 December 20X7.

- C . ST, an entity that was jointly established by AB and CD, and that is accounted for as a joint venture in AB’s financial statements to 31 December 20X7.

- D . AB’s bank that provides more than 60% of the entity’s loan finance.

- E . AB’s main supplier, GH, who supplies more than 70% of AB’s goods for manufacture.

W and Y are very similar entities with the same level of profit before interest and tax.

However, W has gearing of 95% and Y has gearing of 30%.

Which of the following statements is true?

- A . Investing in W carries a higher level of risk than investing in Y.

- B . A greater proportion of profit will be available out of which to declare a dividend in W.

- C . Investors in Y will expect a higher return than investors in W.

- D . Y has a greater commitment to meet interest payments than W.

RS has issued an instrument with a nominal value of $1 million, at a discount of 2.5%, and a coupon rate of 6%. The terms of the issue are that the instrument must either be redeemed at par, at the option of the holder, in three years’ time, or alternatively converted into equity shares in RS.

The characteristics of this instrument taken as a whole indicates that it would be classifed as which of the following?

- A . Compound instrument

- B . Debt instrument

- C . Equity instrument

- D . Discounted instrument

AB and CD are competitors supplying components to the car manufacturing industry. AB operates in Country X and CD operates in Country

Y. Both entities were incorporated on the same day, are the same size and prepare financial statements to 31 March each year using international accounting standards.

Which of the following statements taken individually would limit the usefulness of the comparison of the return on capital employed ratio between the two entities?

- A . The corporate tax rate is 25% in Country X and 40% in Country Y.

- B . The average rate of inflation is 3% in Country X and 10% in Country Y.

- C . The average rate of borrowing is 2% in Country X and 7% in Country Y.

- D . The currency is Dollar in Country X and Krona in Country Y.

Which of the following defines the calculation of interest cover?

- A . Profit before interest and tax divided by finance costs

- B . Finance costs divided by profit before interest and tax

- C . Profit after tax divided by finance costs

- D . Finance costs divided by profit after tax

The consolidated statement of profit or loss for VW for the year ended 30 September 20X7 includes the following:

What is VW’s interest cover for the year ended 30 September 20X7?

- A . 4.5

- B . 3.3

- C . 4.1

- D . 5.1

JJ’s current share price is $1.80, with a dividend of $0.20 a share just about to be paid.

Dividends have increased at an average annual growth rate of 4.5% and this is expected to continue into the future.

What is JJ’s cost of equity?

- A . 17.6%

- B . 16.1%

- C . 12.5%

- D . 11.1%

ST has in issue unquoted 7% debentures which were issued at par and are redeemable in 1 year’s time. These debentures cannot be traded. The yield to maturity on these debentures has been calculated at 5%.

Which of the following would explain why the yield to maturity is lower than the coupon?

- A . ST will benefit from the tax relief on the interest payment.

- B . The debentures will be redeemed at a discount to their par value.

- C . The debentures will be redeemed at their par value.

- D . The market value of the debentures must be higher than their par value.

FG has a weighted average cost of capital of 12% based on its existing:

• level of gearing of 30% (measured as debt/(debt + equity)); and

• business operations.

This would be used as an appropriate discount factor to assess which of the following significantprojects?

- A . A project in an industry in which FG does not currently operate, funded wholly by equity.

- B . A project to extend FG’s existing operations, funded wholly by debt.

- C . A project in an industry in which FG does not currently operate, funded 30% with debt and 70% with equity.

- D . A project to extend FG’s existing operations, funded 30% with debt and 70% with equity.

On 30 November 20X9 OPQ acquires a financial asset that is classified as Available for Sale.

Which of the following describes the value of the financial asset on the date of acquisition?

- A . Fair value excluding transaction costs.

- B . Fair value including transaction costs.

- C . Present value including transaction costs.

- D . Present value excluding transaction costs.

XY purchased $100,000 of quoted 8% bonds in the current year which it intends to hold until redemption.

Which of the following identifies the correct classification and subsequent measurement basis for this financial instrument?

- A . A loans and receivables financial asset subsequently measured at fair value with gains and losses in reserves.

- B . A held to maturity financial asset subsequently measured at amortised cost.

- C . A loans and receivables financial asset subsequently measured at amortised cost.

- D . A held to maturity financial asset subsequently measured at fair value with gains and losses in reserves.

AB sold the majority of its operating equipment to LM for cash on 30 December 20X9 and then immediately leased it back under an operating lease.

AB used the cash proceeds from the sale to reduce its long term borrowings significantly.

No early repayment charge was levied by the lender.

Which of the following statements is true in respect of AB’s ratios calculated at 31 December 20X9?

- A . AB’s return on capital employed would be lower as a result of this sale being recorded.

- B . AB’s current ratio would be lower as a result of this sale being recorded.

- C . AB’s non-current asset turnover would be lower as a result of this sale being recorded.

- D . AB’s gearing ratio would be lower as a result of this sale being recorded.

AB acquired a financial investment on 1 January 20X9, incurring $5,000 related agency fees. AB initially classified the investment as held for trading, in accordance with IAS 32 Financial Instruments: Presentation.

Which of the following statements reflects the accounting treatment that AB adopted in respect of this investment when it prepared its financial statements to 31 December 20X9?

- A . Agency fees were recorded as an expense and the gain/loss on the remeasurement of the investment at the year end was recorded in profit or loss for the year.

- B . Agency fees were recorded as an expense and the gain/loss on the remeasurement of the investment at the year end was recorded in other comprehensive income.

- C . Agency fees were added to the cost of the investment and the gain/loss on the remeasurement of the investment at the year end was recorded in profit or loss for the year.

- D . Agency fees were added to the cost of the investment and the gain/loss on the remeasurement of the investment at the year end was recorded in other comprehensive income.

Ratios calculated from the financial statements of ST Group for the years ended 31 August 20X7 and 20X6 are as follows:

Which of the following would have contributed to the movements in these ratios?

- A . During 20X7 ST Group acquired an associate which made a relatively small profit for the year.

- B . ST Group extended its customer base which resulted in an increase in the volume of sales during 20X7.

- C . During 20X7 ST Group increased the useful life of its vehicles to five years from four and adjusted the depreciation charge accordingly.

- D . The fair value of an investment acquired in 20X7 and classified as fair value through profit or loss has increased in value by the year end.

PQ and WX are similar sized entities and operate in the same industry within Country X. Both operate from a single warehouse and have similar levels of non current asset resources.

The following ratios have been calculated at 31 October 20X8:

If considered individually, which of the following would limit the usefulness of these ratios in assessing the comparative financial performances of PQ and WX?

- A . Depreciation of warehouses being charged to cost of sales by PQ and distribution costs by WX.

- B . Operating lease rentals for plant and equipment being charged to administration expenses by PQ and distribution costs by WX.

- C . Year end review of equipment resulting in WX charging an impairment loss while PQ’s equipment is not impaired.

- D . Increased prices for raw materials, which was passed on to customers by both entities.

CORRECT TEXT

The capital structure of ST issummarised in the table below:

What is the weighted average cost of capital of ST?

Give your answer as a percentage to one decimal place.

? %

A group presents its financial statements in A$.

The goodwill of its only foreign subsidiary was measured at B$100,000 at acquisition.

There have been no impairments to this goodwill.

Exchange rates (where A$/B$ is the number of B$’s to each A$) are as follows:

The value of goodwill to be included in the group’s statement of financial position in respect of its foreign subsidiary for the year ended 31 December 20X4 is:

- A . A$75,758.

- B . A$66,667.

- C . A$150,000.

- D . A$132,000.

Which of the following actions would be most likely to improve an entity’s gross profit margin?

- A . Negotiating with trade suppliers for a bulk purchase discount

- B . Offering increased credit to customers

- C . Reducing administrative expenses by 10%

- D . Writing down the value of obsolete inventories

JK is seeking to raise finance for a project and the directors would prefer to take out a fixed rate bank loan repayable over the next 5 years. The project will increase the profit of JK even after taking into account the additional interest costs.

Which of the following statements about the use of a bank loan in this situation is true?

- A . In the long term servicing a bank loan is more expensive than servicing equity shares due to the higher risk for the lender.

- B . The interest on a bank loan is deducted from profit before dividends can be declared to equity shareholders each year.

- C . Because the assets of a business belong to the equity shareholders, a bank loan should NOT be secured on the assets of the business.

- D . A bank loan has high issue costs compared to an issue of equity shares because it takes longer to arrange.

XYZ had 600,000 ordinary shares in issue on 1 July 20X4. On 1 January 20X5, the entity made a 1 for 2 bonus issue. The profit attributable to ordinary shareholders for the year ended 30 June 20X5 was $2,925,000.

What is the basic earnings per share for the year ended 30 June 20X5?

- A . $3.25

- B . $4.88

- C . $1.63

- D . $3.90

CORRECT TEXT

EF has redeemable 10% bonds which are currently trading at $94.00 for each $100 of nominal value. Thebondscan be redeemed at par in five years’ time. The corporate income tax rate is 22%.

The present value of the cash flows associated with $100 nominal value of these bonds at a discount rate of 7% is $9.28.

Calculate the post tax cost of debt.

Give your answer as a percentage to one decimal place.

%

HJ is currently in dispute with an employee, who is claiming $400,000 in a legal case against them.

HJ’s legal advisors have stated that it is probable that they will lose the case and will have to pay the amount claimed.

Also, HJ are claiming $250,000 from a supplier of defective goods and the legal advisors have stated that it is probable that HJ will be successfulin this claim.

What is the correct accounting treatment for these two items in HJ’s financial statements?

- A . Provide for the $400,000 potential outflow and disclose the $250,000 potential inflow.

- B . Provide for the $400,000 potential outflow and recognise the $250,000 potential inflow.

- C . Disclose the $400,000 potential outflow and disclose the $250,000 potential inflow.

- D . Disclose the $400,000 potential outflow and recognise the $250,000 potential inflow.

What figure will be presented in GHI’s consolidated statement of changes in equity for the year ended 31 December 20X4, in respect of dividends paid to non-controlling interest?

- A . $25,000

- B . $125,000

- C . $100,000

- D . $0

CORRECT TEXT

EF has redeemable 10% bonds which are currently trading at $94.00 for each $100 of nominal value.Thebondscan be redeemed at par in five years’ time. The corporate income tax rate is 22%.

The present value of the cash flows associated with $100 nominal value of these bonds at a discount rate of 7% is $9.28.

Calculate the post tax cost of debt.

Give your answer as a percentage to one decimal place.

%

LM acquired 80% of the equity shares of ST when ST’s retained earnings were $50 million.

The fair value of the net assets of ST included a contingent liability with a fair value of $100 million at the date of acquisition and a fair value of $40 million at 31 December 20X6.

No other fair value adjustments were required at the date of acquisition.

LM and ST had retained earnings of $200 million and $80 million respectively at 31 December 20X6.

The consolidated retained earnings of LM at 31 December 20X6 were:

- A . $164 million

- B . $176 million

- C . $272 million

- D . $284 million