Parker, whose spouse died during the preceding year, has not remarried. Parker maintains a home for a dependent child.

What is Parker’s most advantageous filing status?

- A . Single.

- B . Head of household.

- C . Married filing separately.

- D . Qualifying widow(er) with dependent child.

D

Explanation:

Choice "d" is correct. A qualifying widow (er) is a taxpayer who may use the joint tax return standard deduction and rates (but not the exemption for the deceased spouse) for each of two taxable years following the year of death of his or her spouse, unless he or she remarries. The surviving spouse must maintain a household that, for the whole entire taxable year, was the principal place of abode of a son, stepson, daughter, or stepdaughter (whether by blood or adoption). The surviving spouse must also be entitled to a dependency exemption for such individual. Parker may file as a qualifying widow (er) since her spouse died in the previous tax year, she did not remarry and she maintained a home for a dependent child. Since, qualifying widow (er) is the most advantageous status and Parker qualifies, Parker would file as a qualifying widow (er).

Choice "a" is incorrect. Even though Parker would qualify as single, filing single would give Parker a high tax liability than the qualifying widow (er) status and therefore is not most advantageous. Choice "b" is incorrect. Parker would not qualify as head of household for the first two years after the death of Parker’s spouse because one of the requirements for Head of Household status is that the taxpayer is NOT a surviving spouse. (Also, note that the likely reason for this requirement is that filing as Head of Household status would give the qualifying surviving spouse taxpayer a higher tax liability than the Qualifying Widow(er) status, which would be less advantageous.) Choice "c" is incorrect. Parker would not qualify to file married filing separately.

In which of the following situations may taxpayers file as married filing jointly?

- A . Taxpayers who were married but lived apart during the year.

- B . Taxpayers who were married but lived under a legal separation agreement at the end of the year.

- C . Taxpayers who were divorced during the year.

- D . Taxpayers who were legally separated but lived together for the entire year.

A

Explanation:

RULE: In order to file a joint return, the parties must be MARRIED at the end of the year. Exception: If the parties are married but are LEGALLY SEPARATED under the laws of the state in which they reside, they cannot file a joint return (they will file either under the single or head of household filing status).

Choice "a" is correct. Per the above rule, taxpayers who are married but lived apart during the year are allowed to file a joint return for the year. The fact that they did not live together during the year has no bearing on the issue.

Choice "b" is incorrect. Per the above rule, taxpayers who are married but lived under a legal separation agreement at the end of the year may not file a joint return. They will generally file either under the single or head of household filing status.

Choice "c" is incorrect. Per the above rule, taxpayers who were divorced during the year may not file a joint return together, as they are not married at the end of the year. [Note, however, that they may become married again in the year and file a joint return with the new spouse.]

Choice "d" is incorrect. Per the above rule, taxpayers who were legally separated but lived together for the entire year may not file a joint return. They will generally file either under the single or head of household filing status.

Barkley owns a vacation cabin that was rented to unrelated parties for 10 days during the year for $2,500. The cabin was used personally by Barkley for three months and left vacant for the rest of the year.

Expenses for the cabin were as follows:

Real estate taxes $1,000

Maintenance and utilities $2,000

How much rental income (loss) is included in Barkley’s adjusted gross income?

- A . $0

- B . $500

- C . $(500)

- D . $(1,500)

A

Explanation:

RULE: If a vacation residence is rented for less than 15 days per year, it is treated as a personal residence. The rental income is excluded from income, and mortgage interest (first or second home) and real estate taxes are allowed as itemized deductions. Depreciation, utilities, and repairs are not deductible.

Choice "a" is correct. Applying the rule above, if a vacation residence is rented for less than 15 days per year, it is treated as a personal residence. The rental income ($2,500 in this case) is excluded from income. A Schedule E is not filed for this property (i.e., no income is reported, the taxes are reported as itemized deductions, and the maintenance and utilities are not deductible), so the effect on AGI is zero.

Choice "b" is incorrect. This assumes that the property taxes are reported as itemized deductions but that the rental income ($2,500) less the maintenance and utilities ($2,000) are reported net on Schedule E.

Per the above RULE, the rental income is excluded from income, and the maintenance and utilities are not deductible.

Choice "c" is incorrect. This assumes that all of the items shown are reported net on the Schedule E-$2,500 – $1,000 – $2,000 = ($500). Per the above RULE, the rental income is excluded from income, the maintenance and utilities are not deductible, and the property taxes are reported on Schedule A as an itemized deduction.

Choice "d" is incorrect, per the above rule and discussion.

In evaluating the hierarchy of authority in tax law, which of the following carries the greatest authoritative value for tax planning of transactions?

- A . Internal Revenue Code.

- B . IRS regulations.

- C . Tax court decisions.

- D . IRS agents’ reports.

A

Explanation:

Note: This question is addressed in your Appendix D text materials. We are confident that our students would be able to respond correctly over 85% of the time without any guidance on this topic. The answer is rather obvious. Just by looking at the answer options, you will immediately notice that Option A is presented in title case. This would be a quick sign that it may be the correct response. Further, we suspect that most students would narrow the options down to "a" or "b" by simply using common sense.

While we are confident that our students would fare well on this question if it appeared on their exams, we present the following detailed explanation of the answer options.

Choice "a" is correct. According to the IRS’s website under Tax Code, Regulations and Official Guidance, the "federal tax law begins with the Internal Revenue Code (IRC), [which was] enacted by Congress in Title 26 of the United States Code (26 U.S.C.)." The IRC holds the most authoritative value.

Choice "b" is incorrect. According to the IRS’s website under Tax Code, Regulations and Official Guidance, the IRS regulations or "Treasury regulations (26 C.F.R.)-commonly referred to as Federal tax regulations-pick up where the Internal Revenue Code (IRC) leaves off by providing the official interpretation of the IRS by the U.S. Department of Treasury." Regulations give directions on how to apply the law outlined in the Internal Revenue Code. Regulations have the second most force and effect, second only to the IRC.

Choice "c" is incorrect. Tax court decisions interpret the Internal Revenue Code. They do not have the authority of the IRC.

Choice "d" is incorrect. The reports of IRS agents are used to report on specific taxpayer situations. IRS agents’ reports apply the Internal Revenue Code, IRS regulations, and other forms of authoritative literature, but they do not hold the value that the IRC, the IRS regulations, or even tax court decisions have.

Individual Taxation – Exemptions

In 19X4, Smith, a divorced person, provided over one half the support for his widowed mother, Ruth, and his son, Clay, both of whom are U.S. citizens. During 19X4, Ruth did not live with Smith. She

received $9,000 in Social Security benefits. Clay, a 25 year-old full-time graduate student, and his wife lived with Smith. Clay had no income but filed a joint return for 19X4, owing an additional $500 in taxes on his wife’s income.

How many exemptions was Smith entitled to claim on his 19X4 tax return?

- A . 4

- B . 3

- C . 2

- D . 1

C

Explanation:

Choice "c" is correct. Smith is entitled to an exemption for himself. He is also entitled to an exemption for his mother Ruth (qualifying relative). Ruth has $9,000 in Social Security payments during 19X4, but since that is her only income, the Social Security is not taxable, and nontaxable income does not count in calculating whether an exemption can be taken for a dependent. Clay cannot be taken as a dependent because he filed a joint return with his wife. Since the joint return was filed for a purpose other than simply claiming a refund, the joint return prevents Smith from claiming an exemption for Clay. An exemption cannot be taken for Clay’s wife because she filed a joint return with Clay. Smith is entitled to two exemptions.

Choice "a" is incorrect. Clay cannot be taken as a dependent because he filed a joint return with his wife. Since the joint return was filed for a purpose other than simply claiming a refund, the joint return prevents Smith from claiming an exemption for Clay. An exemption cannot be taken for Clay’s wife because she filed a joint return with Clay.

Choice "b" is incorrect. Clay cannot be taken as a dependent because he filed a joint return with his wife. Since the joint return was filed for a purpose other than simply claiming a refund, the joint return prevents Smith from claiming an exemption for Clay. An exemption cannot be taken for Clay’s wife because she filed a joint return with Clay.

Choice "d" is incorrect. Smith is entitled to an exemption for his mother, Ruth. Ruth has $9,000 in

Social Security payments during 19X4, but because that is her only income, the Social Security

income is not taxable, and nontaxable income does not count in calculating whether an exemption

can be taken for a dependent.

Individual Taxation – Gross Income

Darr, an employee of Sorce C corporation, is not a shareholder.

Which of the following would be included in a taxpayer’s gross income?

- A . Employer-provided medical insurance coverage under a health plan.

- B . A $10,000 gift from the taxpayer’s grandparents.

- C . The fair market value of land that the taxpayer inherited from an uncle.

- D . The dividend income on shares of stock that the taxpayer received for services rendered.

D

Explanation:

Choice "d" is correct. An individual receiving common stock for services rendered must recognize the fair market value as ordinary income. Any dividends received on that stock would also result in income recognition.

Choice "a" is incorrect. Employer-provided medical insurance is a tax-free fringe benefit.

Choices "b" and "c" are incorrect. Gifts and inheritances are both tax-free to the recipient. (Remember tax is often paid by the person giving the gift or the estate at death.)

Adams owns a second residence that is used for both personal and rental purposes. During 2001, Adams used the second residence for 50 days and rented the residence for 200 days.

Which of the following statements is correct?

- A . Depreciation may not be deducted on the property under any circumstances.

- B . A rental loss may be deducted if rental-related expenses exceed rental income.

- C . Utilities and maintenance on the property must be divided between personal and rental use.

- D . All mortgage interest and taxes on the property will be deducted to determine the property’s net income or loss.

C

Explanation:

Choice "c" is correct. Because the second property was personally used more than 14 days, any net loss from the rental of the property will be disallowed.

All related expenses must be prorated between the personal use portion and the rental activity portion.

Prorated depreciation is permitted for the rental activity.

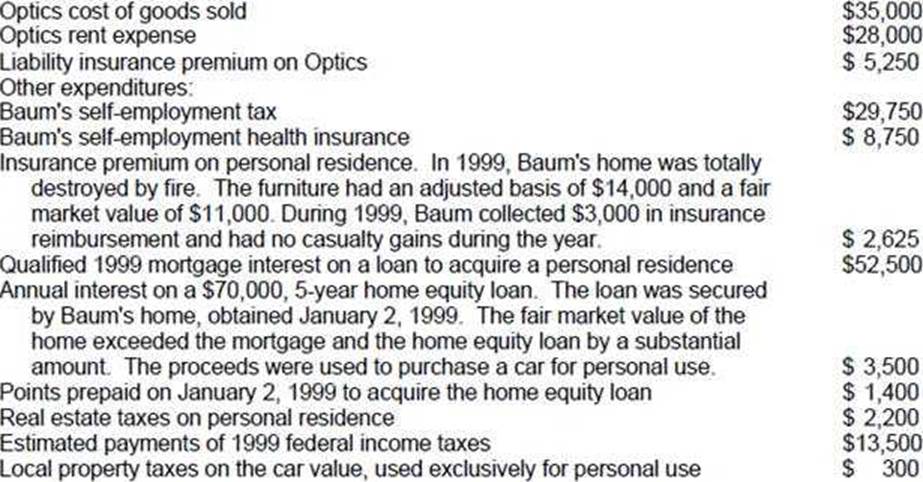

Baum, an unmarried optometrist and sole proprietor of Optics, buys and maintains a supply of

eyeglasses and frames to sell in the ordinary course of business. In 1999, Optics had $350,000 in

gross business receipts and its year-end inventory was not subject to the uniform capitalization rules.

Baum’s 1999 adjusted gross income was $90,000 and Baum qualified to itemize deductions. During

1999, Baum recorded the following information:

Business expenses:

What amount should Baum report as 1999 net earnings from self-employment?

- A . $243,250

- B . $252,000

- C . $273,000

- D . $281,750

D

Explanation:

Choice "d" is correct. Baum should report $281,750 as 1999 net earnings from self-employment (line 12 of the Form 1040), calculated as follows:

Choices "a", "b", and "c" are incorrect. Self-employment tax and self-employment health insurance expenses are adjustments from total gross income. They are not deducted from self-employment earnings (i.e., not reported net on line 12 of the Form 1040).

Note: There are many distracters in this question, all relating to items that are either deductible as part of itemized deductions or not deductible. Be careful to read the requirement of the question before spending unnecessary time on the question. The statement that Baum’s year-end inventory was not subject to the uniform capitalization rules is a distracter as well. There is not enough information given in the facts to apply the rules if he had been subject to them.

On December 1, 1997, Krest, a self-employed cash basis taxpayer, borrowed $200,000 to use in her business. The loan was to be repaid on November 30, 1998. Krest paid the entire interest amount of $24,000 on December 1, 1997.

What amount of interest was deductible on Krest’s 1997 income tax return?

- A . $0

- B . $2,000

- C . $22,000

- D . $24,000

B

Explanation:

Choice "b" is correct. Cash basis taxpayers deduct interest in the year paid or the year to which the interest relates, whichever is later. Even though all of the interest on this loan was paid on December 1, 1997, only the interest relating to December 1997 can be deducted in 1997. The question does not give an interest rate, but because the loan is to be repaid in a lump sum at maturity, 1/12 of the interest, or $2,000 applies to each month.

Choice "a" is incorrect. Because $2,000 of the interest relates to 1997, this amount is deductible in 1997.

Choice "c" is incorrect. This is the amount that cannot be deducted until 1998, the year to which the interest relates. Be sure to read questions like this very carefully, because if you had simply misread the question as seeking the amount deductible in 1998, you would get the question wrong despite understanding the rule.

Choice "d" is incorrect. Cash basis taxpayers can deduct interest in the year paid or the year to which the interest relates, whichever is later, thus 11 months of the interest will not be deductible until 1998.

Which payment(s) is(are) included in a recipient’s gross income?

I. Payment to a graduate assistant for a part-time teaching assignment at a university. Teaching is not a requirement toward obtaining the degree.

II. A grant to a Ph.D. candidate for his participation in a university-sponsored research project for the benefit of the university.

- A . I only.

- B . II only.

- C . Both I and II.

- D . Neither I nor II.

C

Explanation:

Choice "c" is correct.

I. A payment to a student for a part-time teaching assignment is taxable income just as a payment for any other campus job would be. This is not a scholarship or fellowship.

II. There is no exclusion in the tax law for amounts paid to a degree candidate for participation in university-sponsored research.

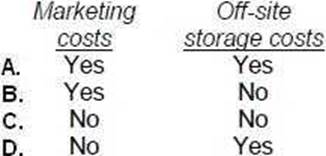

Under the uniform capitalization rules applicable to property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions are met?

- A . Option A

- B . Option B

- C . Option C

- D . Option D

D

Explanation:

Choice "d" is correct. Under the uniform capitalization rules, purchasers of inventory for resale may deduct their marketing costs but must capitalize their off-site storage costs.

Choices "a", "b", and "c" are incorrect. Marketing costs are deductible, but off-site storage must be capitalized.

In a tax year where the taxpayer pays qualified education expenses, interest income on the redemption of qualified U.S. Series EE Bonds may be excluded from gross income. The exclusion is subject to a modified gross income limitation and a limit of aggregate bond proceeds in excess of qualified higher education expenses.

Which of the following is (are) true?

I. The exclusion applies for education expenses incurred by the taxpayer, the taxpayer’s spouse, or any person whom the taxpayer may claim as a dependent for the year.

II. "Otherwise qualified higher education expenses" must be reduced by qualified scholarships not includible in gross income.

- A . I only.

- B . II only.

- C . Both I and II.

- D . Neither I nor II.

C

Explanation:

Choice "c" is correct. Interest earned on Series EE bonds issued after 1989 may qualify for exclusion. One requirement is that the interest is used to pay tuition and fees for the taxpayer, spouse, or dependent enrolled in higher education. The interest exclusion is reduced by qualified scholarships that are exempt from tax and other nontaxable payments received for educational expenses (other than gifts and inheritances).

During 1993 Kay received interest income as follows:

On U.S. Treasury certificates $4,000

On refund of 1991 federal income tax 500

The total amount of interest subject to tax in Kay’s 1993 tax return is:

- A . $4,500

- B . $4,000

- C . $500

- D . $0

A

Explanation:

Choice "a" is correct. Interest income from U.S. obligations is generally taxable. Interest income on a federal tax refund is taxable, even though the refund itself is not taxed.

Choice "b" is incorrect. Interest income on a federal tax refund is taxable, even though the refund itself is not taxed.

Choice "c" is incorrect. Interest income from U.S. obligations is generally taxable.

Choice "d" is incorrect. Interest income from U.S. obligations is generally taxable. Interest income on a federal tax refund is taxable, even though the refund itself is not taxed.

Rich is a cash basis self-employed air-conditioning repairman with 1993 gross business receipts of $20,000. Rich’s cash disbursements were as follows:

What amount should Rich report as net self-employment income?

- A . $15,100

- B . $14,900

- C . $14,100

- D . $13,900

A

Explanation:

Choice "a" is correct. Deductions to arrive at net self-employed income include all necessary and ordinary expenses connected with the business. Estimated federal income tax payments are not an expense. Charitable contributions by an individual are only deductible as an itemized deduction on Schedule A. This assumes the contribution was not made with the "expectation of commensurate financial return."

Choice "b" is incorrect. Charitable contributions are an itemized deduction unless there is an expectation of commensurate financial return.

Choice "c" is incorrect. Federal income taxes paid are not a deductible expense.

Choice "d" is incorrect. Charitable contributions are an itemized deduction unless there is an expectation of commensurate financial return. Federal income taxes paid are not a deductible expense.

On December 1, 1992, Michaels, a self-employed cash basis taxpayer, borrowed $100,000 to use in her business. The loan was to be repaid on November 30, 1993. Michaels paid the entire interest of $12,000 on December 1, 1992.

What amount of interest was deductible on Michaels’ 1993 income tax return?

- A . $12,000

- B . $11,000

- C . $1,000

- D . $0

D

Explanation:

Since Michaels is a cash basis taxpayer, she would deduct the interest expense in the year it was paid. The entire interest amount of $12,000 was paid on December 1, 1992. Therefore, Michaels would have deducted the $12,000 on her 1992 income tax return, not her 1993 return.

Since the interest was already deducted in 1992, there would be no interest deduction for Michaels on her 1993 income tax return, leading to the correct answer of D. $0.

On February 1, 1993, Hall learned that he was bequeathed 500 shares of common stock under his father’s will. Hall’s father had paid $2,500 for the stock in 1990. Fair market value of the stock on February 1, 1993, the date of his father’s death, was $4,000 and had increased to $5,500 six months later. The executor of the estate elected the alternate valuation date for estate tax purposes. Hall sold the stock for $4,500 on June 1, 1993, the date that the executor distributed the stock to him.

How much income should Hall include in his 1993 individual income tax return for the inheritance of the 500 shares of stock, which he received from his father’s estate?

- A . $5,500

- B . $4,000

- C . $2,500

- D . $0

D

Explanation:

Choice "d" is correct. There is no income tax on the value of inherited property. The gain on the sale is the difference between the sales price of $4,500 and Hall’s basis. Hall’s basis is the alternate valuation elected by the executor. This is the value 6 months after date of death or date distributed if before 6 months. The property was distributed 4 months after death and the value that day ($4,500) is used for the basis. $4,500 − $4,500 = 0.

Choice "a" is incorrect. There is no income tax on the value of inherited property.

Choice "b" is incorrect. This is the basis of the stock if the alternate date had not been used. Heirs are not taxed on inheritances. The income or loss results when inherited property is sold.

Choice "c" is incorrect. There is no income tax on the value of inherited property. The gain on the sale is the difference between the sales price of $4,500 and Hall’s basis. Hall’s basis is the alternate valuation elected by the executor.

John and Mary were divorced in 1991. The divorce decree provides that John pay alimony of $10,000 per year, to be reduced by 20% on their child’s 18th birthday. During 1992, John paid $7,000 directly to Mary and $3,000 to Spring College for Mary’s tuition.

What amount of these payments should be reported as income in Mary’s 1992 income tax return?

- A . $5,600

- B . $8,000

- C . $8,600

- D . $10,000

D

Explanation:

Under U.S. federal tax law, alimony payments are generally deductible by the payer and must be included in the recipient’s income. However, the tax treatment of alimony has changed with the Tax Cuts and Jobs Act (TCJA), and this applies to divorce or separation agreements executed after December 31, 2018.

Given that John and Mary were divorced in 1991, the old rules apply.

From the given information:

John paid $7,000 directly to Mary, which would typically qualify as alimony.

John also paid $3,000 to Spring College for Mary’s tuition, and assuming this payment was made as part of the divorce agreement to support Mary, this amount could also be considered as alimony.

Therefore, the total amount that should be reported as income in Mary’s 1992 income tax return is the sum of these payments: $10,000.

Freeman, a single individual, reported the following income in the current year:

Guaranteed payment from services rendered to a partnership $50,000

Ordinary income from a S corporation $20,000

What amount of Freeman’s income is subject to self-employment tax?

- A . $0

- B . $20,000

- C . $50,000

- D . $70,000

C

Explanation:

Choice "c" is correct. Guaranteed payments are reasonable compensation paid to a partner for services rendered (or use of capital) without regard to his ratio of income. Earned compensation is subject to selfemployment tax. Payments not guaranteed are merely another way to distribute partnership profits. The ordinary income reported from an S corporation are taxable income to the individual or their own individual tax return but is not subject to self-employment tax. The ordinary income reported from a partnership may be subject to self-employment tax (if to a general partner).

During 2001, Adler had the following cash receipts:

What is the total amount that must be included in gross income on Adler’s 2001 income tax return?

- A . $18,000

- B . $18,400

- C . $19,500

- D . $19,900

C

Explanation:

Choice "c" is correct. The wages of $18,000 and unemployment compensation are both includable in gross income on Adler’s 2001 income tax return.

Choice "a" is incorrect. The unemployment compensation must be included in gross income.

Choice "b" is incorrect. Municipal bond interest income is excluded from gross income and the unemployment compensation must be included in gross income.

Choice "d" is incorrect. Municipal bond interest income is excluded from gross income.

DAC Foundation awarded Kent $75,000 in recognition of lifelong literary achievement. Kent was not required to render future services as a condition to receive the $75,000.

What condition(s) must have been met for the award to be excluded from Kent’s gross income?

I. Kent was selected for the award by DAC without any action on Kent’s part.

II. Pursuant to Kent’s designation, DAC paid the amount of the award either to a governmental unit or to a charitable organization.

- A . I only.

- B . II only.

- C . Both I and II.

- D . Neither I nor II.

C

Explanation:

Choice "c" is correct. Generally, the fair market value of prizes and awards is taxable income. However, an exclusion from income for certain prizes and awards applies where the winner is selected for the award without entering into a contest (i.e., without any action on their part) and then assigns the award directly to a governmental unit or charitable organization. Therefore, conditions "I" and "II" must be met in order for Ken to exclude the award from his gross income. Choice "a" is incorrect. "II" is a necessary condition as well. See explanation above.

Choice "b" is incorrect. "I" is a necessary condition as well. See explanation above.

Choice "d" is incorrect. "I" and "II" are both necessary conditions. See explanation above.